Financial planning is an essential process that helps individuals and families create a roadmap for achieving their financial goals. In the Indian context, where cultural factors and diverse income levels play a significant role, understanding financial planning becomes even more important. It encompasses various aspects such as wealth accumulation, risk management, and retirement planning, all tailored to meet the unique needs of the individual or family.

The primary objective of financial planning is to accumulate wealth over time through prudent investments and savings strategies. In India, where economic disparities exist, the approach to wealth accumulation may vary significantly from one person to another. Some families may prioritize saving for education or healthcare, while others may focus on creating a substantial retirement fund. By identifying these goals early on, individuals can work towards a balanced financial portfolio that caters to both short-term needs and long-term aspirations.

Risk management is another crucial element of financial planning in India. With the prevalence of unforeseen circumstances such as job loss, medical emergencies, or market volatility, individuals must take steps to protect their finances. This can be achieved through insurance products and creating an emergency fund that provides a safety net in times of need. In addition to protecting against risks, effective financial planning also facilitates informed decision-making, allowing individuals to navigate their finances more confidently.

Retirement planning, particularly in the Indian context, requires careful consideration of various factors. The cultural expectation of familial support during old age may sometimes lead to inadequate preparation for retirement. Therefore, it is essential for individuals to assess their future needs and create a comprehensive retirement strategy that accounts for inflation, rising living costs, and changing lifestyles. By understanding these elements, Indians can achieve long-term financial security and peace of mind.

Setting Financial Goals

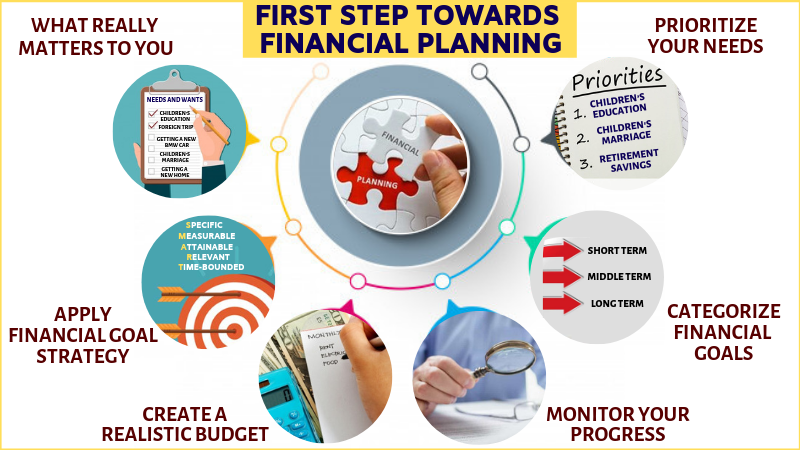

Establishing financial goals is a critical step in the financial planning process. It lays the groundwork for how individuals can approach their finances effectively over time. Setting goals that align with one’s life stage and aspirations requires a clear understanding of the SMART criteria, which stands for Specific, Measurable, Achievable, Relevant, and Time-bound. This structured approach not only enhances clarity but also facilitates better tracking of progress.

Young professionals, for example, might set short-term goals such as saving for a vacation, building an emergency fund, or investing in a small mutual fund. Each of these goals is specific (e.g., saving ₹1 lakh for a vacation), measurable (via bank statements), achievable (with a proper budget), relevant (aligned with their current lifestyle and desires), and time-bound (to be completed within a year). This comprehensive framework ensures that goals are not just ambitious dreams but attainable milestones.

Middle-aged individuals, who may have more pressing financial responsibilities, might focus on investing for retirement, ensuring their children’s education funding, or paying off existing debts. By employing the SMART criteria, they can quantify the amount needed for tuition fees or retirement corpus, creating a roadmap towards fulfilling these significant financial commitments. For instance, calculating the funding required for a child’s college education by setting a target amount to save annually can make planning more manageable.

Families with children may prioritize larger, long-term goals, such as buying a home or saving for family vacations. Here, it is essential to assess each goal’s relevance and allocate resources wisely. The importance of prioritization cannot be overstated, as conflicting financial aspirations can lead to stress and mismanagement. Therefore, evaluating and organizing these goals into short-term and long-term while regularly reviewing them can pave the way for a financially secure future.

Creating a Financial Plan

Establishing a solid financial plan is essential for achieving financial stability and reaching long-term goals. The initial step involves assessing your current financial status. This includes evaluating your assets, liabilities, income, and expenses. Understanding these components will provide a clear picture of your financial health and guide your planning process.

Once you have a grasp of your financial situation, the next step is budgeting. Creating a comprehensive budget allows you to track your spending habits and identify areas where adjustments can be made. It is crucial to categorize your expenses into fixed and variable expenses to manage your finances effectively. A budget serves as a roadmap, helping you allocate resources to necessary expenses while ensuring savings for future investments.

Debt management is another fundamental aspect of a financial plan. It is advisable to list all outstanding debts and prioritize them based on interest rates and payment deadlines. Focusing on high-interest debts first can save money in the long run. Implementing strategies such as the snowball or avalanche methods can also be beneficial in managing and reducing debt effectively.

Investment strategies play a vital role in your financial planning. Understanding the principles of a diversified investment portfolio is crucial. A mix of equity, fixed income, real estate, and mutual funds can mitigate risks and enhance returns over time. Furthermore, an emergency fund should be established, ideally containing three to six months’ worth of living expenses, to safeguard against unexpected financial challenges.

To support your financial planning journey, numerous tools and resources are available for Indians. Online budgeting apps, investment calculators, and financial advisory services can help streamline the process and provide valuable insights. By embracing a structured approach to financial planning, individuals can significantly improve their financial futures, ensuring a stable and prosperous life.

Reviewing and Adjusting Your Financial Plan

Financial planning is not a static process; it requires ongoing attention and adjustment to remain effective over time. Life events such as marriage, the birth of a child, or significant career changes can profoundly impact an individual’s financial circumstances and goals. For instance, getting married may lead to combined finances and shared financial responsibilities, while the arrival of a child introduces new expenses and necessitates considerations for education and healthcare costs. Therefore, it is crucial to periodically review and adjust your financial plan to align it with these changing dynamics.

Tracking your progress is essential to ensure that you remain on course to meet your financial goals. Utilizing various financial tools and metrics can facilitate this process. For example, setting up a budget tracker or using financial planning software can help individuals monitor their spending patterns and savings rate. Assessing whether you are on track to meet your retirement goals or saving adequately for emergencies can provide insights into whether adjustments to your financial strategy are needed. Regularly reviewing your investments and reallocating assets based on performance and market conditions can also enhance the effectiveness of your financial plan.

Additionally, staying informed about financial trends and economic changes in India is vital for implementing successful financial strategies. Economic indicators, changes in government policies, and shifts in the job market can all affect your financial situation. Being proactive about acquiring knowledge on these topics can empower you to adjust your plan in response to emerging risks or opportunities. Seeking guidance from financial advisors may also provide valuable insights tailored to your specific needs and circumstances.

In conclusion, the importance of periodically reviewing and adjusting your financial plan cannot be overstated. By staying proactive and informed, individuals can better navigate their financial journeys, ensuring that they adjust their plans according to life changes and economic conditions.